Categories

Buyer Content, Investing, Seller ContentPublished February 18, 2026

Understanding the Financing Contingency in Your Agreement of Sale

.png)

Understanding the Financing Contingency in Your Agreement of Sale

Deadlines, Termination Rights & Who Gets the Deposit

One of the most misunderstood sections of the Pennsylvania Agreement of Sale is Paragraph 8 – Buyer Financing.

Many buyers believe:

“If I don’t get my mortgage, I automatically get my deposit back.”

Many sellers believe:

“If the buyer can’t get financing, I’m stuck.”

Neither is entirely accurate.

This section of the contract is structured, deadline-driven, and very specific about who can terminate — and when.

Let’s walk through it clearly.

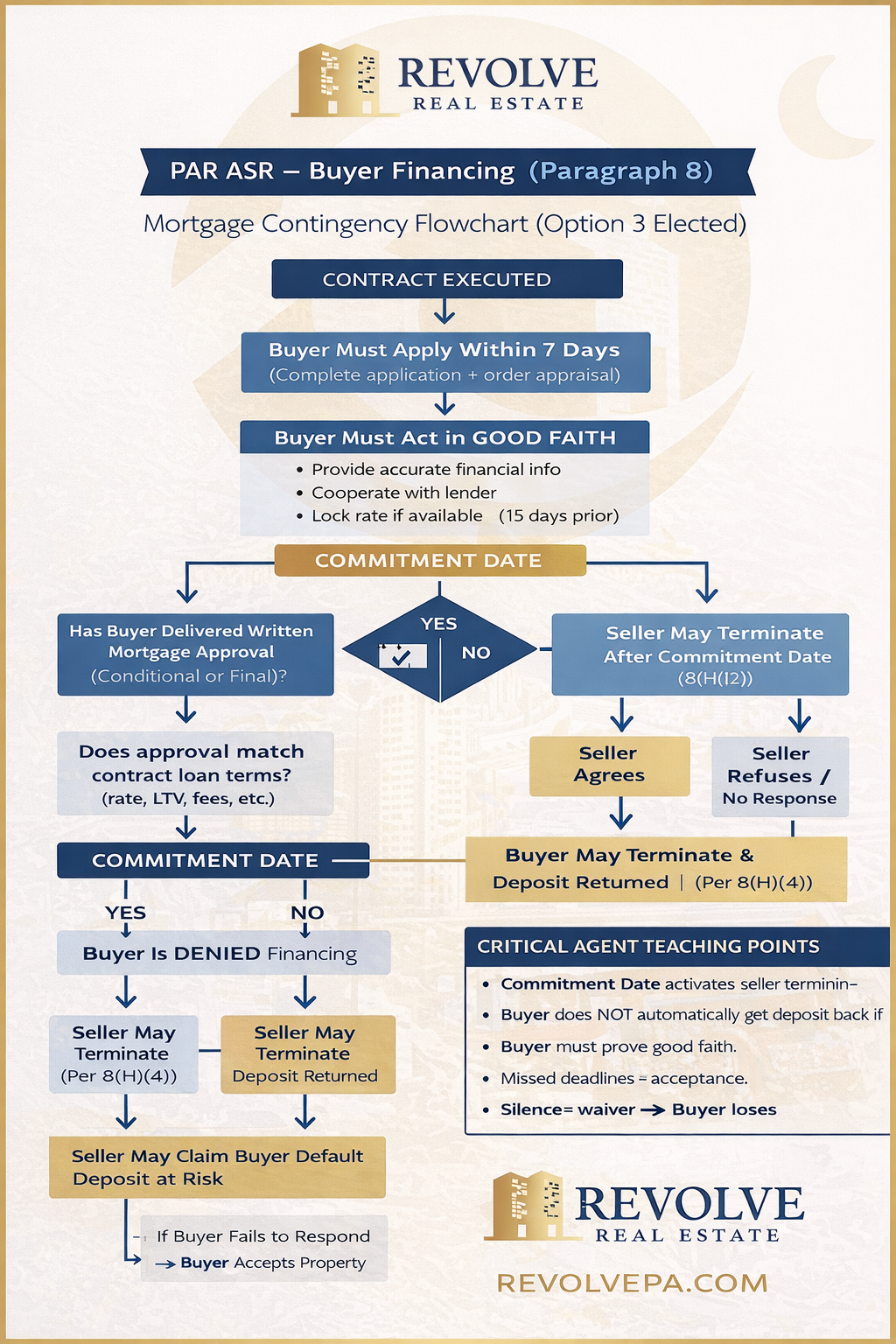

Step 1: The Buyer Must Apply Quickly

Within 7 Days of Contract Execution:

The buyer must:

- Make a complete mortgage application

- Authorize credit checks

- Order the appraisal

- Provide financial documentation to the lender

This is not optional. If the buyer delays applying or fails to cooperate, they may be considered in default.

Step 2: The Buyer Must Act in Good Faith

Throughout the Process, the Buyer Must:

- Provide accurate financial information

- Cooperate with underwriting requests

- Avoid taking on new debt

- Avoid quitting or changing employment

- Lock their interest rate if available (typically required at least 15 days prior to settlement)

If a mortgage is denied because the buyer did something to jeopardize approval, that may be considered bad faith.

Bad faith can put the deposit at risk.

Step 3: The Mortgage Commitment Date (Critical Deadline)

The contract includes a specific Mortgage Commitment Date.

By that date, the buyer must deliver written proof of mortgage approval (either conditional or final).

This approval must:

- Match the loan terms stated in the contract (loan amount, rate cap, type)

- Not include new, unacceptable conditions

This date is extremely important.

It activates termination rights.

What Happens at the Commitment Date?

Scenario 1: Buyer Delivers Proper Approval On Time

The contract continues toward settlement.

The financing contingency is essentially satisfied (though final underwriting still occurs).

Scenario 2: Buyer Does NOT Deliver Approval by the Commitment Date

After the commitment date passes: The Seller May Terminate.

The seller has the right to terminate the agreement if:

-

-

- `No approval is delivered

- The approval doesn’t match agreed loan terms

- Required conditions aren’t satisfied

-

The seller’s termination right continues until proper approval is delivered.

This protects sellers from having their home tied up indefinitely.

Scenario 3: Buyer Is Denied Financing

If the buyer receives a formal denial: The Buyer May Terminate

But only if:

-

-

- The buyer applied on time

- Acted in good faith

- Cooperated fully

-

If properly terminated due to legitimate denial: The buyer’s deposit is returned.

However… If denial appears caused by:

-

-

- Inaccurate financial info

- Failure to provide documents

- Job loss caused by buyer choice

- Taking on major new debt

-

Then the seller may claim buyer default.

In that case:

👉 The deposit may be forfeited.

Scenario 4: Lender Requires Repairs

If the lender requires repairs before approving the loan:

-

-

-

Seller has 5 days to respond.

-

-

Buyer has 5 days to either:

-

Agree to pay for repairs themselves

-

Terminate the contract

If seller refuses:

If the buyer fails to respond within that window: 👉 Buyer is deemed to accept the property as-is.

-

-

-

-

Deadlines matter.

Here Is a Flowchart we Made to Break it Down Visually:

Who Can Terminate — and When?

Here’s the clean breakdown:

| Situation | Who Can Terminate? | What Happens to Deposit? |

|---|---|---|

| Buyer denied loan in good faith | Buyer | Deposit returned |

| Buyer fails to apply / cooperate | Seller may claim default | Deposit at risk |

| Buyer misses commitment date | Seller may terminate | Deposit typically returned unless buyer breached |

| Loan approval doesn’t match terms | Seller may terminate | Deposit returned |

| Lender-required repairs refused | Buyer may terminate | Deposit returned |

| Buyer causes denial | Seller may claim default | Deposit may be forfeited |

Important: Deposit disputes can require mutual release or legal resolution if parties disagree.

Common Misconceptions

❌ “Financing contingency guarantees my deposit back.”

Only if you follow every deadline and act in good faith.

❌ “Seller can’t back out once under contract.”

Seller may terminate if buyer fails to meet financing deadlines.

❌ “If my loan falls apart the week of closing, I’m automatically safe.”

Not necessarily. It depends on whether you complied with all obligations.

What Buyers Should Do

- Apply immediately.

- Respond to lender requests within 24 hours.

- Avoid new credit cards, car loans, or job changes.

- Track your commitment date.

- Communicate with your agent constantly.

The financing contingency protects you — if you perform.

What Sellers Should Do

- Pay attention to the commitment date.

- Request written approval documentation.

- Understand your right to terminate if deadlines are missed.

- Evaluate offers based on financing strength and timeline.

A shorter commitment period can make an offer stronger.

The Bottom Line

The financing contingency is not a loophole.

It is a structured system with:

- Specific deadlines

- Defined performance requirements

- Clear termination rights

- Deposit consequences

Understanding it protects both buyers and sellers.

If you’re preparing to enter into an Agreement of Sale in Pennsylvania, and want to fully understand your rights and obligations, our team at Revolve Real Estate is here to walk you through every detail.

📍 Visit us at www.revolvepa.com

📞 Schedule a consultation before you sign.

or another way